Breaking Down Cost Accounting: Explore Various Types of Costs

Table of Contents

- jaro education

- 27, October 2023

- 4:00 pm

Cost accounting measures all of the expenses connected with manufacturing, including both fixed and variable costs. The goal of cost accounting is to aid management in decision-making processes that optimise operations based on efficient cost management. In the area of cost accounting, understanding different types of costs is crucial. It enables businesses to manage expenditures carefully with proper analysis.

PGDM programs provide valuable lessons on cost accounting to help them manage their accounts. The Online PGDM Program offered by the Loyola Institute of Business Administration (LIBA) caters specifically to professionals seeking to enhance their career prospects without disrupting their work commitments. This online program is recognised globally and adheres to an immersive and collaborative teaching methodology.

Understanding Cost Accounting

Cost accounting is the process of recording all the expenses associated with the production of a product or service. It basically implies keeping track of your spending to make sure that you have a profitable earning. Cost accounting helps you determine how much it costs to manufacture a product, which in turn is useful in determining how much to charge. If you know how much your raw materials cost and how much labour is involved in manufacturing your product, you can calculate how much profit you will make on each item sold. Evaluate the profit and see if it is worthwhile to produce that item. It also estimates future costs and earnings based on historical trends.

Types of Cost Accounting Methods

Cost accounting is a part of financial management, helping businesses to analyse and manage their expenses effectively. Different cost accounting methods fall into four main categories. Each category is suited for specific business needs. We outlined these methods with their key characteristics and when to use them.

1. Standard Cost Accounting

- Meaning: Standard cost accounting compares actual costs with budgeted or standard costs to assess a company’s profitability. It uses predetermined standard costs as benchmarks for evaluating performance.

- Benefits: Businesses can use this tool to track budget consistency, uncover expense inconsistencies, and make informed decisions. Standard cost accounting helps in the identification of inefficiencies and the control of expenses.

- Drawbacks: Requires significant managerial effort to establish and maintain standard costs. This may necessitate additional resources to implement effectively.

- When to Use: Standard cost accounting is suitable to use when a company has a clear understanding of its production costs and aims to monitor cost efficiency continuously. It is also useful for identifying process improvements.

2. Activity-Based Costing (ABC)

- Meaning: The cost of a product or service is assigned using activity-based costing, based on the actions required to produce it. It provides a more accurate picture of cost allocation and overhead expenses.

- Benefits: Enhances cost transparency by breaking down costs by specific activities. Helps identify cost-reduction opportunities and improves inter-departmental communication.

- Drawbacks: Implementation can be complex and time-consuming due to data analysis and modelling requirements. Does not consider fixed costs or overhead expenses.

- When to Use: Appropriate when the data on activity costs related to products or services is available from all relevant departments. Useful for pinpointing areas of cost optimization.

3. Job Costing

- Meaning: Job costing tracks costs associated with individual projects or jobs. It allows companies to compare actual costs against planned costs for specific tasks or projects.

- Benefits: It helps in determining the goal by comparing actual costs with planned costs for each job. It identifies opportunities for improvement in the process.

- Drawbacks: Job costing requires a detailed record of employee time and expenses on each job, which can be challenging for remote or non-standard work environments.

- When to use: It is effective when precise cost information is needed to make decisions about specific projects or actions. This type of costing is valuable for businesses dealing with multiple small projects or varying customer orders.

4. Process Costing

- Meaning: Process costing breaks down the cost of producing a product into individual steps or processes. It is often used in manufacturing, where products have multiple components.

- Benefits: It offers details about cost allocation for each component or process, which helps companies with high fixed and low variable costs understand cost.

- Drawbacks: Process costing does not consider external factors like competition or demand. So, tracking all production steps accurately can be challenging and lead to departmental focus on the bigger picture.

- When to use: Process Costing is suitable when a company has high fixed and low variable costs as understanding the cost impact of changing prices is crucial.

This type of cost accounting is commonly used in manufacturing for detailed cost analysis of product components.

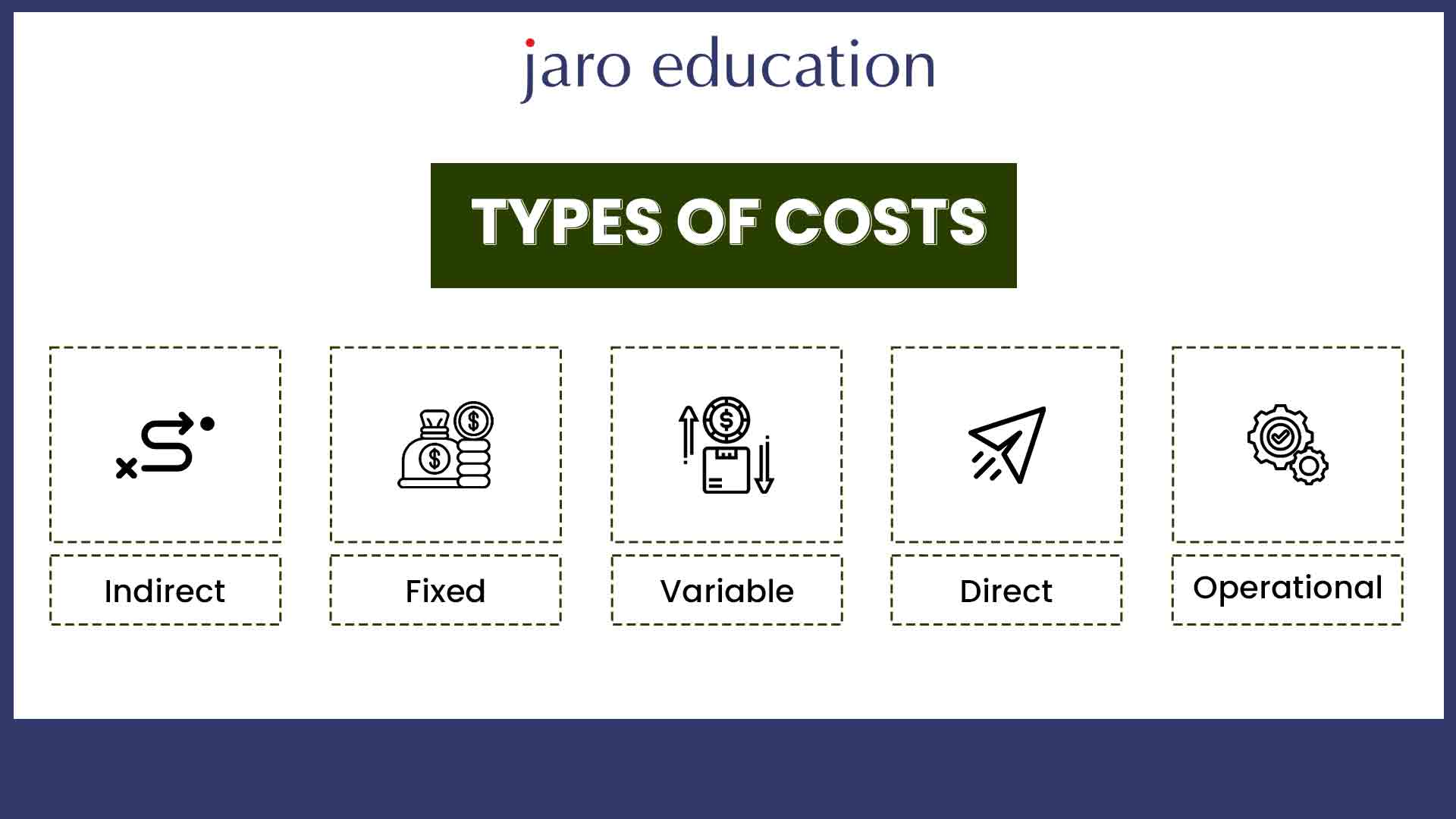

Different Types of Costs

The different types of cost in cost accounting are as follows:

*tickertape

Direct Costs

The most frequent kind of expenses a company may have is direct costs. It represents the direct expenses incurred during manufacturing a good or making avail of any of the services. Raw materials required to make a product, labour costs, and any transport or distribution fee are examples of direct costs. Direct costs for a producer of vehicles, for instance, would be the price of the raw materials and metals as well as the salaries of the workers involved in making the cars.

Indirect Costs

Indirect costs are charges that have no immediate connection to the manufacture of a certain product or activity. These costs cannot be easily traced to a particular department or project. For example, electricity used to power the car manufacturing and production factory is considered as an indirect cost associated with creating cars as there is no direct link of this expenditure exclusively with production because the auto company consumes electricity for every aspect of its business.

Fixed Costs

Fixed costs, also referred to as overhead costs which remain constant regardless of fluctuations in production. These expenses include rent for office or facility space, salaries of employees inclusive of payroll taxes and benefits, insurance against potential losses, and interest on loans borrowed, which maintains a steady rate irrespective of variations in production levels. These unchanging costs are integral to a business’s operational stability and are not subject to shifts based on the volume of products manufactured or services rendered.

Variable Costs

Variable costs vary in direct proportion to changes in production output. As production increases, variable costs rise, and they decrease when production decreases. Packaging costs for a toy manufacturer are an example of variable costs. For instance, a toy maker must wrap its toys before sending them to retailers. This is a sort of variable cost because, as the toy producer makes more toys, its packaging costs rise. On the other hand, if less toys are being produced, the variable cost related to the packaging would definitely fall.

Operating Costs

Operating costs, also known as operating expenses, encompass day-to-day expenses necessary to run a business but aren’t directly linked to a specific product. Examples include rent and utilities for a manufacturing facility. Operating cost and indirect costs, or costs related to real manufacturing, are categorised separately. Investors can determine a company’s operating expense ratio, which demonstrates how well it uses costs to produce sales.

Opportunity Costs

It refers to the benefits forfeited when one choice is made over another. In investing, it represents the difference in return between chosen and foregone investments. For businesses, opportunity costs help in decision-making, even though they don’t appear on financial statements. For example,a business chooses to purchase a brand-new piece of manufacturing machinery instead of leasing it. So here the difference between the cost of the machinery investment and higher production and the amount of money that could have been used to reduce debt instead of purchasing the equipment to save money on interest costs is known as the opportunity cost.

Sunk Costs

Sunk costs are historical expenses that cannot be recovered, yet firms are not required to take them into account when making future financial choices. New equipment costs and marketing campaign expenses are examples of sunk costs. The company can’t get this money back, but by spending it, it can make profits.

Controllable Costs

Business managers have the authority to increase and decrease controllable expenses. Bonuses, donations to charities, office supplies, and staff gatherings can all be considered controllable expenses. Managers and entrepreneurs have complete control over these costs and may decide how much money they spend on each one. While they spend on various events, it is imperative to manage these costs and maintain a proper track of them, so that every expense is diligently recorded for future reference.

Importance of Cost Accounting

Cost accounting plays a vital role in business operations, benefiting various stakeholders including employees, clients, investors, and governmental bodies. Here are some key advantages of cost accounting:

Informed Financial Decision-Making

Cost accounting distinguishes between fixed and variable expenses, enabling informed financial decisions. Management can set product prices based on production costs, ensuring profitability.

Performance Recognition

Cost accounting assesses individual work efficiency, fostering a competitive work environment. Efficient employees receive timely recognition and incentives and stay motivated.

Cost Management and Control

By analysing various costs incurred in running a company, cost accounting aids in cost management and control. It identifies opportunities to reduce operational expenses, leading to improved efficiency, which benefits both the company and its clients.

Differences Between Cost Accounting and Financial Accounting

Here is a detailed comparison of cost accounting and financial accounting:

Audience and Focus

- Cost Accounting: Primarily targets the company, its management, and employees. It helps in internal decision-making.

- Financial Accounting: Focuses on external stakeholders such as lenders, investors, and the public. It provides financial information for external reporting and compliance.

Applicability

- Cost Accounting: Typically used by industrial enterprises and organisations with production processes. It helps in optimising internal operations.

- Financial Accounting: Used by all types of businesses, including service and retail industries. It helps in accurate financial reporting for external parties.

Nature of Costs

- Cost Accounting: Considers both predetermined (budgeted) and historical costs. It focuses on cost types, helping in cost allocation and control.

- Financial Accounting: Primarily deals with historical costs. It records financial transactions and presents them in financial statements.

Forecasting and Budgeting

- Cost Accounting: Utilises budgeting strategies to predict and forecast expenses, facilitating proactive cost management.

- Financial Accounting: It focuses on past financial data and does not involve forecasting or budgeting.

Conclusion

Cost accounting has a prime role when it comes to making financial decisions for businesses. From allocating resources to improving profitability, it has a multi-faceted importance. By understanding various types of costs and their interplay within an organisation, companies can effectively manage their finances and meet their financial goals.

Enroll for the online PGDM program by Loyola Institute Of Business Administration through Jaro Education and learn various aspects of business, including cost accounting. This course is designed to be equivalent in stature to full-time MBA programs. Joining this insightful program will introduce you to a vibrant community of learners, leaders, and change-makers, while you learn how various cost types play different roles in shaping financial decisions.

Trending Blogs