- jaro education

- 6, May 2024

- 10:00 am

Finding your way into the complex world of entrepreneurship necessitates a thorough understanding of financial fundamentals. Among these, break-even analysis is an essential tool for entrepreneurs, providing invaluable insights into the dynamics of profitability and sustainability. In this comprehensive guide, we will study the details of break-even analysis, decipher its principles, and provide entrepreneurs with the tools they need to make informed decisions. From deciphering fixed and variable costs to understanding the significance of the break-even point, this blog is a guide for both aspiring and experienced entrepreneurs, illuminating the path to financial understanding and success in the constantly evolving world of business.

Understanding the Break-Even Analysis

Break-even analysis serves as a vital financial tool for companies to determine their Break-Even Point (BEP). It remains an internal management instrument, typically not shared with external stakeholders such as investors or regulators. However, financial institutions might request it for financial projections in a bank loan application. The calculation considers both fixed and variable costs relative to unit price and profit.

Fixed costs, which stay constant irrespective of sales volume, encompass expenses like facility rent or mortgage, equipment costs, salaries, interest on capital, property taxes, and insurance premiums. Variable costs, on the other hand, fluctuate with changes in sales. These include direct hourly labour payroll costs, sales commissions, and expenses for raw materials, utilities, and shipping. Variable costs represent the combined labour and material costs required to produce one unit of your product.

Table of Contents

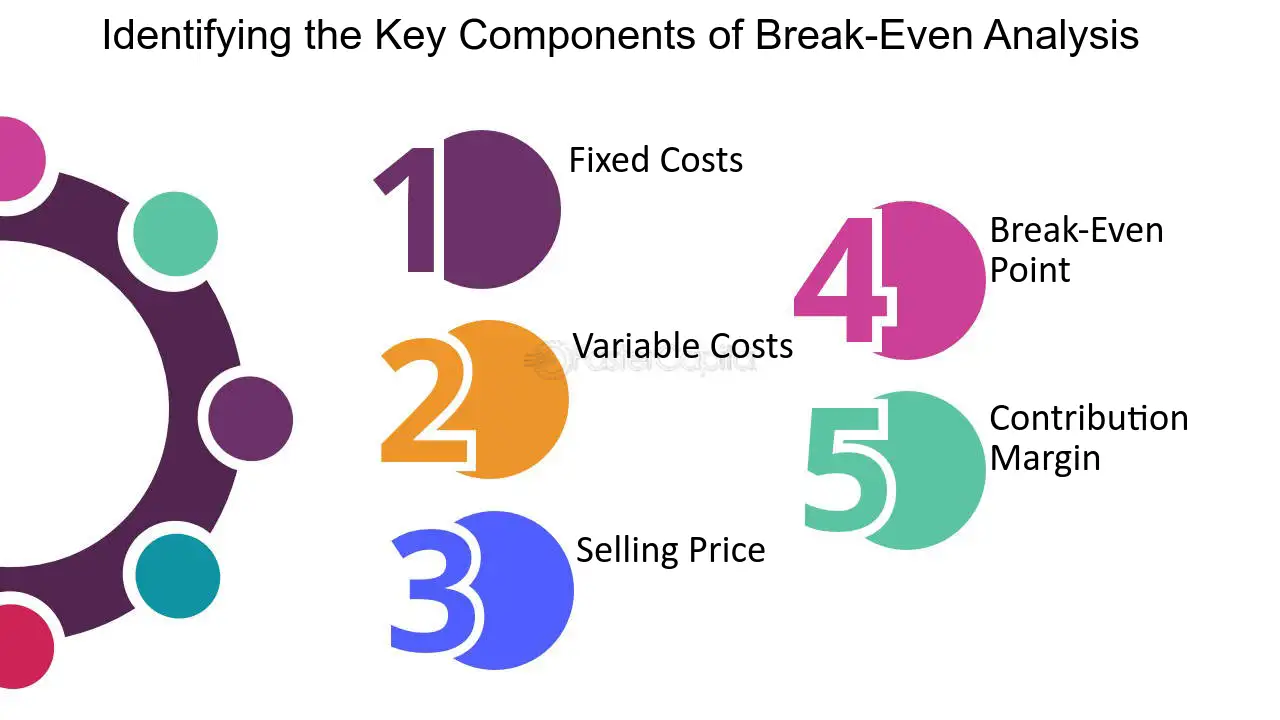

Key Components of Break-Even Analysis

The key components of break-even analysis are as follows:

Understanding Cost Structure

Break-even analysis begins with a thorough understanding of a business’s cost structure, which involves categorising costs into fixed (e.g., rent, salaries) and variable (e.g., raw materials, production costs). Analysing the cost structure provides entrepreneurs with valuable insights into the financial implications of their business operations.

Evaluating Revenue Streams

An essential aspect of break-even analysis is assessing a business’s revenue streams, including product sales, service fees, or subscription models. This evaluation helps entrepreneurs determine the necessary sales volume or customer base required to cover costs and reach the break-even point.

Break-Even Point

The break-even point signifies the level of sales or revenue at which a business neither earns a profit nor incurs a loss. It serves as a critical metric in break-even analysis, guiding entrepreneurs in setting achievable sales targets and making informed decisions regarding pricing, production volume, and marketing strategies.

Contribution Margin

The contribution margin represents the difference between the selling price of a product or service and its variable costs. It indicates the revenue available to cover fixed costs and contribute towards profit. Analysing the contribution margin enables entrepreneurs to evaluate the profitability of various products or services and make strategic decisions concerning pricing and cost management.

Sensitivity Analysis

Sensitivity analysis is a technique used within break-even analysis to assess the impact of changes in key variables on the break-even point. By conducting sensitivity analysis, entrepreneurs can understand how variations in factors like sales volume, pricing, or costs influence the financial viability of their business. This analysis helps identify potential risks and opportunities, facilitating proactive decision-making.

*fastercapital.com

How to Calculate Break-Even Point?

To calculate the break-even point, you can use the following formula:

Break-Even Point (in units) = Fixed Costs / (Selling Price per Unit – Variable Cost per Unit)

Here’s how to calculate it step by step:

- Determine your fixed costs: These are expenses that remain constant regardless of the number of units produced or sold. Examples include rent, salaries, insurance, and utilities.

- Determine your variable costs per unit: Variable costs are expenses that vary with the level of production or sales. Examples include raw materials, labour, and shipping costs.

- Determine your selling price per unit: This is the price at which you sell each unit of your product or service.

- Plug the values into the formula: Divide your fixed costs by the difference between the selling price per unit and the variable cost per unit.

- Calculate the break-even point: The result will give you the number of units you need to sell to cover all your costs and break even.

Remember that the break-even point can also be calculated in terms of sales revenue instead of units by multiplying the break-even point in units by the selling price per unit.

Knowing the Uses of Break-Even Analysis

The methods of break-even analysis serve as a fundamental financial tool for both established businesses and startups, offering insights into financial performance and aiding effective budgeting. Here’s an elaboration on the four key uses of break-even analysis:

1. Assessing Profitability

The primary function of break-even analysis is to determine whether a business is breaking even or incurring losses. By identifying the break-even point, businesses can understand the revenue needed to achieve profitability. Moreover, it provides clarity on the adjustments required, whether increasing revenue or reducing costs, to attain profitability. Amidst various methods to gauge profitability, calculating the break-even point stands out for its simplicity and clarity.

2. Informing Future Budgets

Break-even analysis proves invaluable for entrepreneurs and fledgling companies grappling with decisions on product offerings, sales volumes, and budget allocations. This analysis facilitates decision-making by quantifying the necessary sales volume for profitability and estimating the longevity of products. Adjusting variables such as fixed costs, sales price, and volume metrics enables businesses to formulate precise budgets for each cost component.

3. Mitigating Financial Risks

Small businesses are inherently exposed to risks, particularly concerning product launches and withdrawals. Break-even analysis helps in risk assessment by revealing insights before significant decisions are made. For example, if projected demand falls short of the break-even sales volume, launching the product might not be financially viable. Identifying the break-even point offers clarity on which risks are worthwhile, enhancing decision-making processes.

4. Ensuring Accurate Pricing

Once the break-even point is determined, businesses can strategically adjust pricing to achieve profitability. By understanding the required sales volume and revenue per unit, businesses can assess whether current pricing aligns with break-even objectives. If the break-even point cannot be met at the existing price, it signals a need for price adjustments. This is particularly beneficial for businesses stuck in pricing stagnation or those navigating initial pricing decisions.

Advantages of Break-Even Analysis

Many small and medium-sized businesses overlook meaningful financial analysis, often unaware of the necessary sales volume to generate returns on their capital.

Planning and Decision-Making Power

Break-even analysis serves as a potent tool for planning and decision-making, providing critical insights into costs, quantities sold, prices, and more, which are essential for informed business strategies.

Smarter Pricing Strategies

Understanding the break-even point aids in devising more effective pricing strategies. While psychology plays a role in pricing, comprehending its impact on gross profit margins is equally vital to ensure bills can be paid.

Covering Fixed Costs

Beyond variable costs, businesses must cover fixed expenses like insurance or web development fees. Conducting a break-even analysis ensures these costs are accounted for, contributing to overall financial stability.

Identifying Missing Expenses

Break-even analysis prompts businesses to thoroughly outline their financial commitments, reducing the likelihood of surprises and overlooked expenses in the future.

Setting Sales Targets

By determining the sales volume required for profitability through break-even analysis, businesses can set tangible sales targets for themselves and their teams, fostering clarity and focus in achieving financial goals.

Facilitating Informed Decision-Making

Relying solely on emotion can lead entrepreneurs astray. Break-even analysis empowers decision-making with factual data, enabling entrepreneurs to make informed choices based on tangible evidence.

Limiting Financial Strain

Break-even analysis acts as a risk mitigation tool, aiding in discerning when to avoid pursuing a business idea to prevent failures and minimise financial strain, fostering a realistic understanding of potential outcomes.

Securing Business Funding

Integral to any business plan, break-even analysis is often a prerequisite for attracting investors or securing loans. Demonstrating the viability of the business plan through analysis instils confidence in potential investors and lenders, facilitating access to necessary financing.

Limitations of Break-Even Analysis

Break-even analysis is a valuable tool for financial management and decision-making, yet it possesses limitations that restrict the breadth of information it can provide. They are as follows:

Not a Predictor of Demand

It’s crucial to recognise that break-even analysis does not predict demand. While it indicates the sales volume required for profitability, it does not forecast actual sales or consumer demand, offering only a threshold for operational profitability.

Dependence on Reliable Data

Break-even analysis relies on accurate data for meaningful results. However, complexities arise when costs overlap between fixed and variable categories, requiring careful categorisation. Inaccurate data input can compromise the reliability of break-even calculations.

Simplicity

The break-even formula oversimplifies complex business scenarios, particularly for businesses with multiple products and varied pricing structures. This limitation necessitates working with one product at a time or estimating average prices, potentially leading to less nuanced analysis.

Static Model

The analysis assumes static conditions, disregarding fluctuations over time and in response to changes in prices and costs. Weekly or seasonal variations in sales are overlooked, requiring supplementary tools like cash flow management and sales forecasts for a comprehensive understanding.

Lack of Future Consideration

Break-even analysis lacks foresight into future changes, such as potential increases in raw material costs or shifts in market dynamics. Failure to account for future variables can lead to inaccuracies in break-even projections and hinder strategic planning.

Neglect of Competitive Factors

The analysis overlooks the influence of competitors on market dynamics, pricing strategies, and demand fluctuations. Changes in competitor actions, such as price adjustments or supply chain disruptions, can impact a business’s break-even point and profitability.

Conclusion

Break-even analysis stands as a fundamental pillar of financial management for entrepreneurs, offering a thorough understanding of profitability and operational dynamics. Throughout this guide, we have understood the intricacies of break-even analysis, from deciphering fixed and variable costs to exploring its applications in pricing strategies, budgeting decisions, and risk mitigation.

By grasping the key components of break-even analysis and acknowledging its limitations, entrepreneurs can leverage this powerful tool to make informed decisions, set realistic goals, and navigate the complex terrain of business with confidence. Join IIM Nagpur’s Post Graduate Certificate Programme in Product & Brand Management and unlock the potential of managing brands and products. Through this 10-month-long course, individuals can indulge in live classes mentored by experienced faculty associated with IIM Nagpur. By availing a rigorous pedagogy they can make themselves ready for the real-world job market. Furthermore, they have an extensive opportunity of peer networking for widening their scope in the field.

Trending Blogs